We use cookies to improve the user experience on our website, target contents and marketing and develop our website. Some of the cookies are necessary for the website to function properly while others help us provide you with better services when you visit our website. You can read more about cookies or change your choices later on the Cookies page. The link to the page can also be found at the bottom of the site.

Scam messages related to pensions circulating in the name of pension companies

Do not open links in the text messages. Delete the message. If you are unsure whether the message you received is genuine, you can contact Varma's customer service.

Large employer's TyEL contribution and contribution category

As a large employer, the amount of your TyEL contribution is affected by your company's payroll and contribution category. The fewer disability pensions your employees are granted, the lower your company's contribution category and TyEL contribution will be.

Large employer's TyEL insurance contribution

In 2025, your company is considered a large employer if it paid more than EUR 2,337,000 in wages to its employees in 2023.

A contribution category is determined for a large employer, and it affects the amount of the disability pension component of the TyEL contribution. If your company's payroll in 2023 was less than EUR 2,337,000, no contribution category will be determined for 2025.

What is a contribution category?

As a large employer, your company will always belong to one of the contribution categories. The contribution category is determined by your company's disability risk and affects the amount of the TyEL contribution.

There are 11 contribution categories in total, with the lowest contribution category being 1 and the highest 11. Contribution category 4 is the basic category, in which the disability risk corresponds to the average level of the earnings-related pension system.

The contribution category affects the contribution as follows:

Contribution categories 1 to 3 reduce the contribution.

Contribution categories 5 to 11 increase the contribution.

How is the contribution category determined?

The contribution category, and therefore the disability contribution, is affected by the disability pensions of your company's employees. The contribution category is always calculated in advance for the following year on the basis of realised pension expenditure.

Pension expenditure refers to the amount of money needed to pay an employee's disability pension on average until the lowest retirement age. The amount of pension expenditure depends on the age of the employee, the amount of the pension and the duration of the disability.

The contribution category is determined by the risk ratio calculated for it. The risk ratio is calculated by comparing your company's disability pension expenditure to the average disability pension expenditure. If your company's pension expenditure is higher than the average pension expenditure, the risk ratio is higher and the contribution category is higher.

The risk ratio is calculated as the average of the risk ratios from two and three years ago. For example, the contribution category for 2025 is determined by the average of the risk ratios calculated for 2022 and 2023. It is therefore affected by the disability pension expenditure from 2022 and 2023.

What impact does the contribution category have?

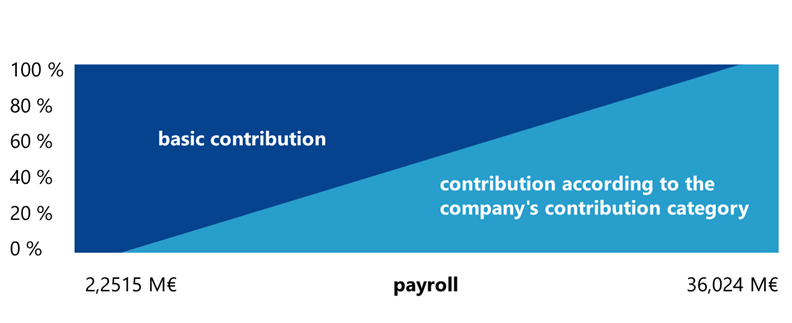

Your company's payroll has an impact on how much the contribution category affects the TyEL contribution. The higher the payroll, the higher the so-called liability level and thus the higher the impact on the disability contribution.

The liability level determines how much of the disability contribution is a basic contribution based on the age structure of the employees and how much is a contribution based on the contribution category.

In 2025, a company's liability level can range between 0-90%. If a company's liability level is 60%, for example, 60% of its disability contribution will be based on the contribution according to the contribution category. If your company's payroll exceeded EUR 37,392,000 in 2023, your company's contribution rate is 90% in 2025.

The contribution category and the liability level may change as a result of business restructuring.

The liability level rises as the payroll increases. The larger the company, the more its disability pensions contribute to the disability contribution through the contribution category.

The contribution category can be influenced through work ability management

You can influence your company's contribution category by taking care of your employees' work ability, because the fewer disability pensions your employees are granted, the lower your company's contribution category and TyEL contribution will be. Varma offers you reliable expertise and effective tools to help you manage your employees' work ability and identify disability risks.

Varma Academy is a free e-learning platform where you can find online courses, webinars and ready-to-use learning paths on developing and maintaining work ability management, designed for supervisors, HR professionals and employees alike.

The contribution category model used to finance disability pensions was reformed at the beginning of 2024. The aim of the reform is to encourage employers to ensure timely and effective disability prevention and rehabilitation.

The TyEL contribution includes a contribution loss component to cover the credit losses caused by unpaid pension contributions to the earnings-related pension company. As a large employer, you get a discount on the contribution loss component, known as the contribution loss reduction.

How is the contribution loss component reduction determined?

The contribution loss reduction is a percentage of the TyEL payroll, and its amount depends on the amount of the payroll. The contribution loss reduction percentage for 2025 is determined according to the amount of the payroll paid in 2023.